Explore AI's impact on accounting: applications, benefits, and future trends. Join Ultralytics in shaping AI innovation!

Explore AI's impact on accounting: applications, benefits, and future trends. Join Ultralytics in shaping AI innovation!

Accounting is one of the most important parts of running a business. It’s the systematic process of recording, analyzing, and reporting financial transactions. You can think of accounting as the business's GPS. It helps them speed up success, avoid bumps in the road, and stay on the right track legally.

However, accounting can often be tedious and time-consuming. That’s where AI can step in. AI can help accountants reduce their workload and save lots of time. In this ultimate guide, we'll take a look at how AI is changing accounting and making tasks easier for accountants.

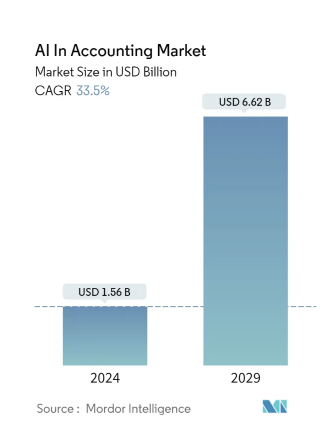

Artificial intelligence is making big changes in finance. According to a report by Mordor Intelligence, the market value of AI in accounting is expected to reach an impressive $6.62 billion by 2029. This surge is driven by AI's ability to enhance accuracy and efficiency across various accounting tasks.

KPMG, a top accounting firm, conducted a survey. They found that 59% of 500 C-suite executives are already using AI for taxes and finance. Also, 40% of them want to invest more than $10 million in it in the next 12 months. This quick growth proves that people in finance see AI's value. It can make hard tasks easier, manage money better, and help accountants.

Let’s walk through a few applications of AI in accounting.

Accounting is changing quickly with new technology, like machine learning and deep learning. These changes are making accounting more automated. This makes tasks like data entry and bookkeeping easier and more efficient.

Technologies like Robotic Process Automation (RPA) can do tasks like tracking expenses automatically. An RPA bot can recognize and sort various types of receipts on its own. It can also put together expense reports and paychecks by using the data it gathers. Plus, these bots can sign into accounts, record bank transactions, and make bank reconciliation statements without help.

AI in accounting can also offer instant data analysis and reporting. Companies can watch their finances in real-time, quickly seeing changes in cash flow, spending, and income. This means they can make faster decisions. Businesses can spot and respond to new chances or problems right away.

How does this work? AI tools use advanced algorithms to process and analyze financial data instantly. Through this AI analysis, trends, anomalies, and patterns that might go unnoticed by human eyes can be spotted. Also, by learning from the data it processes, the AI system can improve over time and provide fast and accurate financial insights.

Truewind and Docyt are examples of AI tools that can help with real-time data analysis and $reporting. Truewind automates accounting with machine learning, making reports and transaction categorization fast and accurate. Docyt simplifies bookkeeping, providing real-time views of finances to help manage expenses and profits easily.

By using AI, accountants can tap into vast amounts of data to accurately predict future financial trends and outcomes. These advanced tools sift through past financial records, market trends, and even global economic indicators to provide precise forecasts. This means businesses can fine-tune their financial strategies based on these forecasts.

Also, predictive analytics can help spot possible financial discrepancies or fraud early on. It does this by scanning financial data for unusual patterns that could hint at errors or fraud. By catching issues earlier, businesses can have a higher level of financial security.

Artificial intelligence is changing how audits are done. AI helps auditors dig deeper into the data they check, leading to better risk assessments. Recent studies have shown that AI boosts both the quality and speed of audits. Platforms like AuditFile use AI and machine learning algorithms to help auditors complete audits faster and with fewer risks. With AI, auditors can complete their work faster and with increased confidence in the accuracy of their findings.

We explored various applications of AI in accounting, ranging from automating repetitive tasks to streamlining auditing processes. Next, let's understand how these applications benefit the accounting industry.

AI simplifies and automates time-consuming manual tasks like data entry, reconciliations, and invoice processing, ensuring high accuracy. For example, PwC, a global professional services firm, implemented AI solutions in the finance processes of a leading luxury hotel chain.

This implementation resulted in a remarkable 27% increase in efficiency and streamlined operations. As a result, the hotel can do its work faster and with fewer mistakes. Staff members also gain the opportunity to focus more on important tasks that require human attention.

Analyzing large datasets in real-time can provide stakeholders with vital insights for making informed decisions. For example, Deloitte, a global professional services firm, used a special method to optically extract data from thousands of commercial loan documents for a financial sector M&A deal. This technology helped them avoid doing 4,000 hours of manual work. With this AI solution, they could analyze data faster and more accurately. As a result, they made better decisions, saved money, and completed tasks more quickly.

AI plays an important role in protecting financial assets and ensuring their integrity. Tools like Amazon Fraud Detector use AI to detect suspicious transactions and anomalies in real time. This results in a drastic decrease in fraud attempts and substantial financial savings for businesses.

By using AI-driven solutions, organizations can proactively identify and address potential threats. Companies can keep their money and customer information safer. Plus, customers feel more secure doing business with them. They know that their transactions are being watched over for any signs of fraud.

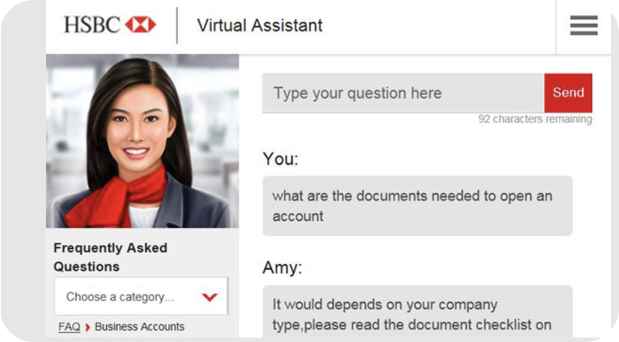

Companies like HSBC use chatbots to handle customer inquiries without needing to call a call center. This means customers get more personalized advice and stay loyal. When AI chatbots and virtual assistants are combined, customer interactions get even better, leading to happier customers overall.

This approach saves time for both the company and the customers. It also makes help available anytime. It makes it easier for customers to get the support they need - whenever they need it.

Integrating AI into accounting helps save money. AI automates simple tasks like entering data and checking transactions. This means less manual work and fewer people needed, which cuts costs. AI can work all day without mistakes, making financial reports faster and more accurate. Fewer errors also mean less chance of losing money. Overall, using AI in accounting makes things cheaper and more efficient for businesses.

People worry that AI might replace accounting jobs, but the truth is simple. Human skills like thinking and being creative are hard to automate. Ultimately, human accountants are needed to make important decisions. While AI might change some office jobs, it's not taking over everything. In fact, accounting jobs are expected to grow by 4% in the next ten years, which is even more than the average job growth.

On the other hand, AI is actually creating jobs in accounting. Analysts from the World Economic Forum (WEF) say automation will create 58 million new jobs, and most of these will need high skills. Even though AI can do routine tasks, accountants with special skills are needed to make sense of the data AI collects. They can offer better advice because of this.

Looking ahead, AI and new tech are set to make a big impact on accounting. They're going to make things faster, safer, and more personalized. Let's dive into some exciting trends that are changing how accounting works:

It’s clear that the accounting field is quickly evolving with AI. Bots that can handle banking and smart auditing tools are emerging. Embracing AI in your business's accounting processes can save time by automating routine tasks.

This freed-up time can be invested in strategic analysis. AI is key to navigating our technology-driven future. It's redefining how we work and innovate. AI is transforming traditional practices into dynamic and efficient systems.

At Ultralytics, we are excited to push the boundaries of AI. Take a look at our GitHub repository to explore our latest contributions to artificial intelligence. From healthcare to agriculture, we're actively involved in innovating with AI! 🌟🚜